Chip Industry Series: Memory Chip 1

"It turns out that you are wearing a cycle of high-tech outerwear, well, then take the money to kill the opponent, and you will die if you don't believe it!"

——Cong T

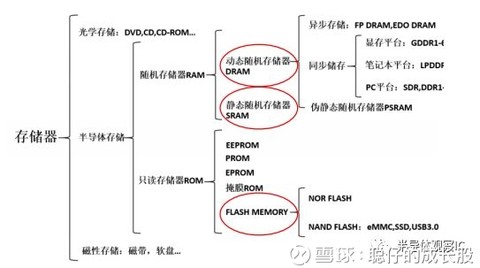

The memory chip is a component for storing programs and data. For a computer, if there is a memory, there is a memory function to ensure normal operation. There are three main categories of memory classification: optical storage, magnetic storage, and semiconductor storage. At present, the mainstream memory is the semiconductor memory chip. In the semiconductor memory classification, the memory chip can be divided into two categories according to whether the data is lost after power-off. One type is non-volatile memory. After this type of memory chip is powered off, Data can be stored, mainly represented by NAND Flash, commonly found in U disk and SSD (solid state hard disk); the other type is volatile memory. After this type of memory chip is powered off, data cannot be stored, mainly represented by DRAM. In the computer, mobile phone memory.

In simple terms, DRAM is the memory we usually use, and NAND Flash flash, the thing it is doing is actually the hard disk.

In addition to NAND Flash and DRAM, semiconductor memory chips include other categories such as Nor Flash and SRAM. However, from the analysis of output value, NAND Flash and DRAM are the core components of the memory chip industry, accounting for 37% and 57% of the output value respectively. According to WSTS data, the global semiconductor memory market reached US$124 billion in 2017, accounting for 30% of global semiconductor production.

According to the latest report from IC Insights, the market research organization, the total value of the global DRAM memory chip industry is expected to reach 101.6 billion US dollars in 2018, an annual increase of 39%, ranking first, accounting for 24% of the entire IC industry. At the same time, this will be the first time in history, and the value of the IC industry in a single field has exceeded the $100 billion mark. The output value of the NAND flash memory industry is expected to reach 62.6 billion US dollars, and the memory industry totals 164.2 billion US dollars, accounting for 38% of the entire industry.

In front of so much nonsense, I just want to explain the memory chips that I have to explain today.

Memory and hard disk

At the beginning of the article, writing to DRAM is the memory used by our usual computer or mobile phone, and NAND Flash is equivalent to a computer hard disk or a mobile hard disk. What is the difference between hard disk and memory? The computer hard drive capacity is clearly 1TB, but why is it running very slowly?

The difference between the hard disk and the memory is that the data stored in the chip will not be retained after the power is turned off. Even if the power is turned off, the data of the hard disk will not disappear.

But when the computer CPU wants to calculate data, if the CPU wants to read data directly from the hard disk, the time will be too long. Therefore, the memory will act as a "middle bridge", first copying a copy into the hard disk, and then letting the CPU directly read the data in the memory to do the operation. This will be about a million times faster than reading data directly from the hard drive.

Open the task manager, you can see the memory space occupied by the program currently in execution. Many people are consuming high computational resources in Chrome. The memory usage is higher than other browsers, and more than a few pages of memory are eaten. It’s over. So in a nutshell, a computer is just like an office, drinking a drink, reading a book, listening to an audio... The more you use it, the bigger the desktop (memory). But things that are not used in the other time will be placed in the drawer (hard disk). So even if the hard disk is bigger, you want to perform many tasks at a time, you still have to look at the memory size. The memory is processed faster than the hard disk, but the data disappears after the power is turned off, and the price is also more expensive than the hard disk. Therefore, under the same conditions, two other mobile phones or computers with almost identical hardware configurations, the larger the DRAM, the faster the running speed.

Andy Beer's law

In the 1990s, under the leadership of Intel CEO Andy Grove and Microsoft CEO Bill Gates, the two companies formed the "Wintel Alliance", Intel provides Microsoft with powerful performance. The processor, while Microsoft is constantly upgrading the Windows system to squeeze the performance of the processor. The popular saying at the time was:

"What Andy gives , Bill takes away."

This is the famous "Andy Beer's Law"

To this day, this law is still playing an active role: Why is it that the old iPhone of the previous two years will not be able to get up to the latest system? Because the new iOS system needs more powerful performance support, and the configuration of the old iPhone is not enough. So, every other year or two, you will have the idea of renewing your new phone and new computer.

With the advancement of systems and software, the demand for memory for mobile phones, computers and other devices is greater. In 2018, the mainstream Android flagship, 6GB of memory is now standard, some domestic phones are even equipped with 8GB of memory; and iPhone 8 and iPhone X are also equipped with 3GB of memory - and when the iPhone was first released in 2007, the memory is only 128MB.

For decades, Andy Beer's Law has been driving the boom in the notebook and mobile phone markets.

The best financial products in 2017 - memory

What is the best financial product in 2017? Certainly many people will think of the house, and they will not think of the stock of A shares when they die. The memory stick becomes the best financial product of the year. Yes, it is the following thing. Take the current mainstream Kingston Hacker's Fury series as an example. In late October 2017, the price of a single 8GB DDR4-2400 on Suning has reached 1197 yuan, which is 4 times the historical lowest price of 288 yuan a year ago. many.

At present, the memory that is relatively expensive is mainly referred to as Dynamic Random Access Memory (DRAM), which belongs to volatile memory;

The game "Play Battle Grounds", which is popular in the world for "winner winner, chiken dinner", requires 8GB of memory for the official recommended configuration. If you want to play the top screen with the highest special effects, then 32GB of memory is essential, optical memory I have to spend more than 4,000 oceans - I can't afford to eat chicken.

Recently, there is such a paragraph: "Opening the Internet in 2016, bought more than 400 DDR4 8GB memory modules, a 180-speed block. In 2017, the Internet cafe lost more than 100,000. Yesterday I sold all the Internet cafes. The second-hand memory stick sold 600, which actually earned me the money to open the Internet cafe."

The reason for the price increase of memory

Andy gives, Bill takes away, pointing out that even if hardware evolves faster, it is always consumed by software, causing hardware to constantly upgrade performance to meet software requirements. Conversely, the output of high-performance hardware will not be able to cope with the demand for software, resulting in a situation of short supply.

In 2016, the price of memory and flash memory continued to decline. The manufacturers complained, but in the second half of the year, the form went down sharply. All the way up, not only the price increase was high, but also the duration also created a record. What is the reason behind this. Around this incident, various conspiracy and conspiracy have also arisen. It is said that supply is in short supply. It is said that Samsung, SK Hynix, Micron and other manufacturers have colluded. What are the reasons for this round of big price hikes?

1: Market trends have changed, demand for mobile devices has increased

In the past few years, everyone has been talking about the PC market. In addition to the gaming PC market, there are some other things in the market. The sales in other markets have declined. The mobile market has also recovered from the Blue Ocean to the Red Sea. The growth rate has also slowed down, but the manufacturers’ Competition has not stopped, but in order to increase the attractiveness and continue to push up the configuration. In the past two years, the smartphone memory has increased rapidly from the previous 2-3GB to 6GB. The flagship machine even went up to 8GB of memory, and the flash memory capacity has changed from the previous 16GB, 32GB to 64GB, and the high-end point even went to 128GB. 256GB storage. Not only the Android camp, but also Apple's iPhone and iPad. The phone has 3GB of memory, the iPad Pro memory has been greatly increased to 4GB, and the storage capacity is also 64GB, 128GB and 256GB. Last year's iPhone 8 and iPhone X were even more awkward, directly 64GB. 256GB two capacities, 128GB are canceled.

Considering that Apple's iPhone has more than 200 million sales per year, the storage capacity has doubled, and the impact on the overall market demand is very large. Domestic manufacturers have also joined the competition. The low-end mobile phone memory and flash memory capacity are all in the competition. Great growth, 6+64GB is the basic configuration of the entry.

The mobile market is the main cause of this round of DRAM memory price increase. In addition, the memory sales of the server and data center market are also increasing. The demand for the entire memory chip market is rising against the trend. Although the PC market is declining, it cannot change the general trend. After all, the sales of mobile devices have already surpassed the PC market, so the price increase of PC memory is largely due to the shackles of the fish. The DIY players are home to this time.

2: Process conversion progress is unfavorable and capacity is affected

Market demand has soared. The normal practice of supply chain manufacturers should be to increase productivity to meet market demand, but they have lost their chains at such an important juncture. In 2016, Samsung, Micron, SK Hynix, Toshiba and other manufacturers are facing technology upgrades - memory shifts to processes below 20nm, flash memory is also moving from 2D flash to 3D flash, and stack layers are constantly being upgraded, but this process is not smooth, leading to vendors The production capacity has not increased rapidly.

Taking memory as an example, Samsung is the earliest mass production 20nm process. In early 2016, it announced the 18nm process. The normal plan is to mass production at the end of 2016. However, the 18nm process is not as good as expected. Earlier, the 18nm memory chip yield was not good. The news of the emergency recall, despite Samsung’s official denial, has cast a shadow over the new process. In addition to Samsung, SK Hynix, Micron because of capital, technical strength is not as good as Samsung, 20nm, 18nm process conversion process is more difficult than Samsung.

According to the data released by IC Insights, the bit capacity growth of DRAM memory chips in 2017 is only 15-20%. This growth is only a drop in the bucket compared to market demand. It cannot change the situation of short supply, which leads to the market being under-supplied. The price naturally rises.

3: Memory manufacturers, distributors hoarding, secondary exploitation

The upstream manufacturers' capacity and downstream demand are the key to determining the price increase of the memory. However, in this price increase disaster, the upstream manufacturers are not the only culprit, and the entire industry chain manufacturers are participating in the price increase. The price increase is a big earn.

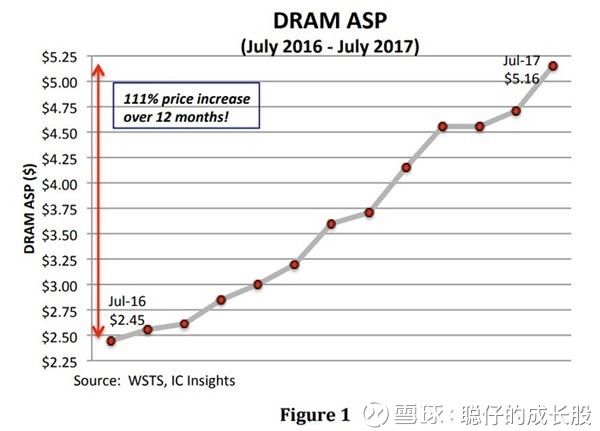

According to the statistics of Jibang Technology, from July 2016-July 2017, the price increase of DDR4 memory granules is about 111%, but the price increase of memory sticks can be more than that. In the first half of 2016, DDR4 memory is sold for 8GB. The price is about 200 yuan, but the price of 8GB memory sticks in 2017 broke through 600 yuan, 700 yuan or even 800 yuan mark, reaching 1197 yuan in late October.

From here we can also see that the upstream price increase of memory particles is only a part of this price increase, and memory manufacturers and distributors are also indispensable in this process. The more the supply is insufficient and the selling price is increased, the more manufacturers are unwilling to ship, but the hoarding is even more ambiguous. Some dealers are also the same, and there is no goods at hand. The gambling is that prices continue to rise, while manufacturers and dealers are The restrictions on shipments have further increased market vacancies, thus forming a vicious circle.

4: The timing of the subtle factory accident, behind the price increase

There is another factor that can't be ignored for the price increase of the memory chip. Originally it was only a small probability event. It will never affect the overall situation in normal times, but it has become very sensitive now. This is a factory accident. At that time, SK hynix Wuxi fire and Thailand floods affected the price trend of memory and hard disk. This scene appeared from time to time in this wave of price increases, including the power outage of Samsung Xi’an NAND factory, nitrogen pollution of Micron Taiwan factory, Toshiba 10 Ten thousand wafers are scrapped and so on. The funny thing is that the official attitude of the manufacturers has always been soothing, indicating that accidents will not seriously affect production capacity and will not lead to market vacancies, but these things are widely spread without exception, artificially spread memory, flash memory and price increases. The news led to market panic.

These accidents will not have much impact on the usual situation. However, in the current situation, a small number of accidents may be exploited by people and become an excuse for out-of-stocks and price increases. The ordinary people are unable to refute this and can only accept 挨slaughter.

History of DRAM industry development

After several decades of cyclical cycles in the DRAM field, players have gradually reduced from 40 to 50 in the 1980s to five before the 2008 financial crisis: Samsung (Korean), SK Hynix (Korean), and Qimonda. (German), Magnesium (US) and Elpida (Japan), five companies basically control the global DRAM supply, and end product manufacturers such as Kingston, almost no DRAM production capacity, they must purchase raw materials from them.

Although the memory industry looks very high-tech, very tall, but the product price trend is similar to that of chemical products, strong cyclical, big ups and downs, rising prices to count the amount of money, the whole body trembles, killing the price to go crazy and even slashing themselves.

In a strong cyclical industry, there are usually several characteristics:

1. The degree of product standardization is high, the user is weak, who is cheap to buy;

2. The industry has economies of scale, and large-scale production can effectively spread low prices;

3. Heavy assets, huge depreciation, once the production can not stop, the loss must also be hard to produce scalp, at least there is cash flow;

4. The industry pattern is still unstable. There is no price alliance. When the price increases, the manufacturers want to expand their production to kill their opponents. When the valley is low, they will achieve capacity through bankruptcy and merger.

The memory meets all of the above features.

Samsung has taken full advantage of the strong cycle characteristics of the memory industry, relying on the government's blood transfusion, when prices fall, overproduction, and other companies cut investment, the market is expanding wildly, and the price of products is further reduced through mass production, thus competing for competitors. Exiting the market and even going bankrupt, the world calls it the "counter-cyclical law." In the field of memory, Samsung has sacrificed three "counter-cyclical laws". The first two occurred in the mid-1980s and early 1990s, allowing Samsung to start from scratch and achieve the position of the memory leader. However, Samsung obviously felt that it was not big enough to play, so it played a counter-cyclical expansion for the third time before and after the 2008 financial crisis.

At the beginning of 2007, Microsoft introduced the Vista operating system that madly eats memory. DRAM vendors judged that memory demand will increase greatly, so they have increased their production capacity. As a result, Vista sales fell short of expectations. DRAM oversupply prices plummeted, and the 2008 financial crisis worsened. DRAM particles Prices range from 2.25 dollars to abrupt to 0.31 dollars. At this time, Samsung made a jaw-dropping move: Putting 118% of Samsung's total profit in 2007 into the DRAM expansion business, deliberately aggravating the industry's losses, and putting the last straw on the tough competitors.

The effect is significant. The price of DRAM has flown down all the way. In 2008, it fell below the cost of cash. At the end of 2008, it fell below the cost of materials. At the beginning of 2009, the third German manufacturer Qi Mengda could not hold it first and declared bankruptcy. The memory players in continental Europe disappeared. At the beginning of 2012, the fifth Elpida announced bankruptcy. Japan, which once occupied more than 50% of the DRAM market, also lost its last card. On the night of the announcement of the bankruptcy of Elpida, the Samsung headquarters of Gyeonggi Province was clear all night, and the stock price soared the next day. The whole world knows that the Koreans won this time.

At this point, there are only three players left in the DRAM field: Samsung, Hynix and Micron. After the bankruptcy of Elpida, the company’s new CEO’s Micron Technology was packaged at more than $2 billion in 2013. The $2 billion is really a jump in prices. Five years later, the market value of magnesium has risen from less than $10 billion to 46 billion. The $2 billion is almost the same day's amplitude.

Remember these three giants, although they usually compete with each other, but when it comes to making money, it is a consumer who immediately wears a pair of pants and partners in the world. Technology, capacity, and market are all in their hands. So how much do they want to produce and how much they want to sell? Others can't control it, and once they find out that there are competitors, these will be stunned and jointly kill the new challenger in the cradle. Among them, the most embarrassing is Samsung in South Korea.

DRAM market structure

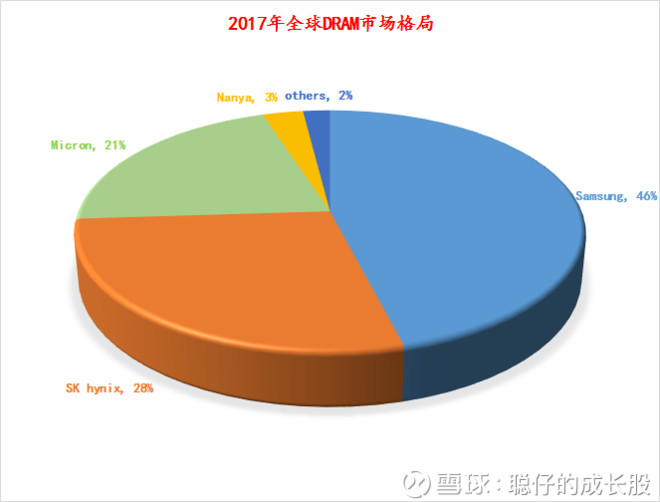

Since Micron announced the acquisition of Japan's Elpida in 2012 and successfully completed the acquisition a year later, the global DRAM market has entered the pattern of Samsung, SK Hynix and Micron's three oligarchs. According to DRAM EXchange data, the DRAM market is dominated by Samsung, Hynix and Micron. The market share of Samsung is about 46%, and the market share of Samsung + Hynix + Micron is as high as 95%.

Under the monopoly of foreign-funded manufacturers, Chinese mobile phone and notebook manufacturers such as Huawei, ZTE, Xiaomi and Lenovo often encounter DRAM out-of-stock situations. In China, only SMIC has a small amount of DRAM capacity, and it is impossible to achieve import substitution.

How to do it? Have money to buy it? In July 2015, China Ziguang Group made a $23 billion takeover offer to Micron Technology, the world's third largest DRAM maker. The result was rejected by Micron on the grounds that the US government would block the deal with information security concerns.

So from 2016, China has set off a storm of investment in the DRAM industry. Ziguang Group announced that it will invest USD 24 billion to build a national storage base in Wuhan (Wuhan Xinxin Phase II 12-inch wafer DRAM factory), covering an area of more than 1 square kilometer. The first phase of 2018 will have a monthly production capacity of 200,000 pieces, which is expected to be 2020. It has a monthly production capacity of 300,000 pieces and an annual output value of more than 10 billion US dollars. It is planned to build a monthly capacity of 1 million pieces in 2030. Fujian Jinhua Group cooperated with Taiwan Lianhua Electronics to invest 37 billion yuan in the first phase to build a 12-inch wafer DRAM factory in Jinjiang. In 2018, it will build a monthly production capacity of 60,000 pieces and an annual output value of 1.2 billion US dollars. It is planned to build 240,000 pieces per month in the fourth phase of 2025. Hefei Changxin invested 49.4 billion yuan (7.2 billion US dollars), and built 205,000 pieces of monthly production capacity in 2018.

In January 2017, Ziguang Group announced an investment of 30 billion US dollars (about 200 billion yuan), invested in building a semiconductor storage base in Nanjing, Jiangsu Province, the first phase of investment of 10 billion US dollars, built a monthly capacity of 100,000, mainly producing 3D NAND FLASH (flash) , DRAM memory chip.

The total investment of the above four projects exceeded US$66 billion (445 billion yuan).

The history of the DRAM industry will make people see one thing

- Take the money to kill the opponent, and a little less will die! Do not believe that all are dead!